Before you invest in an ETF, it’s worth looking under the hood. Here’s what you can find out if you go deeper than a fund’s fact sheet.

Exchange-traded funds (ETFs) have become tremendously popular investment vehicles for do-it-yourself investors. Today, there are more than 4,300 ETFs offered on Canadian and U.S. exchanges by firms that issue, manage and market them.

Like mutual funds, ETFs are regulated by provincial and territorial securities commissions, which regulate their sale and distribution. This includes requirements for disclosing investment information and pricing. ETF sponsors must provide and update several different reports, such as ETF Facts sheets and prospectuses. Seasoned investors can and should use the information in these regulatory documents to evaluate individual ETFs.

This article gives a brief overview of these financial reports and documents—all free and readily available to the Canadian public—and explains how investors can use the information to make decisions on which ETFs to buy or sell.

ETF sponsors are required to disclose and update several different reports.

ETF reports are updated regularly:

Investors can locate these financial reports directly on the ETF sponsor’s website. For example, National Bank Investments lists all regulatory documents, and you can access a specific ETF Facts sheet, prospectus, financial report or proxy voting record.

Note that an individual ETF’s prospectus and financial statements are often bundled together with those of other ETFs offered by the fund sponsor.

Bobby Argitis, business development manager with National Bank Direct Brokerage, says the ETF Facts sheet is the most useful of the brochures because it highlights key information that most investors are looking for, such as the management expense ratio, investment objective, top holdings and performance. “Most DIY investors can find everything they need in the ETF Fund Facts sheet summary,” he says.

Argitis adds that other useful information, such as the liquidity of an ETF, can be gleaned by looking at the total assets of the fund, the average daily trading volume and the average bid-ask spread. Smaller ETFs are not traded as frequently as larger ETFs and can have a wider spread between the bid and ask prices—adding to the total cost for buying and selling the ETF.

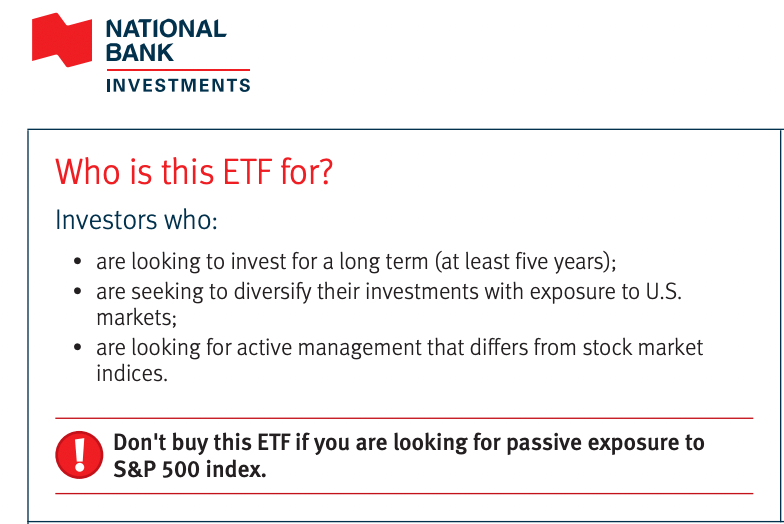

Looking through an ETF’s financial reports and disclosures is a good way for keen investors to dig deeper and expand their knowledge. It might even prevent a case of mistaken ETF identity. For instance, an investor eager to invest in a U.S. equity ETF might miss the word “active” in the NBI Active U.S. Equity ETF (NUSA/TSX). A quick scan of the ETF Facts sheet shows a helpful warning not to buy this ETF if you are looking for passive exposure to the S&P 500 index.

The proxy voting records can also be an interesting source of information. The same NBI Active U.S. Equity ETF holds shares of Microsoft Corporation (MSFT/NASDAQ). NBI voted for a shareholder proposal to provide a report on the gender and racial pay gap, as well as on the effectiveness of workplace sexual harassment policies, even though Microsoft management recommended a vote against these proposals. (Visit NBI for full details about its ETFs.)

Financial reporting and disclosures offer investors a wealth of information that go beyond the basics of fees and performance. They allow investors to look under the hood at the fund’s financials and uncover useful facts about the fund’s structure, holdings, tax implications, pricing, trading volume and even proxy voting records.

While the ETF Facts sheet provides investors with most of the information they need to evaluate an ETF purchase, some of the more exotic ETFs may require a deeper dive to understand their inner workings and how they impact you as an investor.

Your investing platform can be a great resource. National Bank Direct Brokerage has a dedicated ETF Centre that helps users search for funds based on industry, management style, annual fees and more. Investors can also improve their skills with a wide range of articles, videos, tutorials and seminars. National Bank Direct Brokerage also has a free mobile app for iOS and Android. On your smartphone or tablet, you can trade stocks and ETFs online at $0 commission, create watchlists, set up alerts for specific stocks, transfer funds and more.

MoneySense ranked National Bank Direct Brokerage as the best online broker for ETF investing in 2021 and 2022. Use the promo code MoneySense when you open an account* and you’ll pay no commissions on transactions.

This is a paid post that is informative but also may feature a client’s product or service. These posts are written, edited and produced by MoneySense with assigned freelancers.

Robb Engen is a fee-only advisor who will work with you to achieve your financial goals by creating a financial plan with actionable steps along the way.

Practical advice on how to build your retirement savings for employees at mid-career, the self-employed, single parents and more.

Boomers admit they had it easier than others, but Gen Z gave themselves a C in paying off debt.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

It’s hard but not impossible for those raising kids on their own to plan and save for retirement without.

Seniors seeking a decumulation strategy may be asking the wrong questions. Start with your spending plan, then model how.

Canada cuts rates again. Can Couche-Tard take over the convenience-store world? Mag 7 outperformance trend may be done. Dollarama.

the MoneySense Finder tool at her work-from-home desk" width="300" height="180" />

the MoneySense Finder tool at her work-from-home desk" width="300" height="180" />

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out.

Many 30-year-olds are at the crossroads of some major life expenses. Here’s how to save for retirement during a.

Sure, VFV could be a good buy, but there are U.S. ETFs with even lower fees available for Canadian.

MoneySense, Canada’s personal finance resource for 25 years, is owned by Ratehub Inc., but remains editorially independent. The editorial team works to provide accurate and up-to-date information, but details can change and mistakes could happen. We encourage readers to do their own research, practice critical thinking and compare their options, especially before making any financial decisions. If you read something you feel is incorrect or misleading, please contact us. MoneySense is not responsible for content on external sites that we may link to in articles. We aim to be transparent when we receive compensation for advertisements and links on our site (read our full advertising disclosure for more details). Advertisers/partners are not responsible for and do not influence our editorial content. Our advertisers/partners are also not responsible for the accuracy of the information on our site. Be sure to review product information as well as provider terms and conditions on their sites. (Products and offers may vary for Quebec.) The content provided on our site is for information only; it is not meant to replace advice from a professional.